If you already own a home in Fairfax, moving up can feel like a balancing act. You want to protect the equity you have built, buy your next home with confidence, and avoid the stress of carrying too much risk at once. The good news is that with the right timing plan, you can make smart decisions in a market that is still active and tight on inventory. Let’s dive in.

Fairfax timing starts with local facts

Before you map out a move-up plan, make sure you know whether your home is in Fairfax County or the City of Fairfax. They are separate jurisdictions, and that affects local tax rules, payment dates, and how you should interpret market data. You can confirm local tax details through the City of Fairfax tax information page.

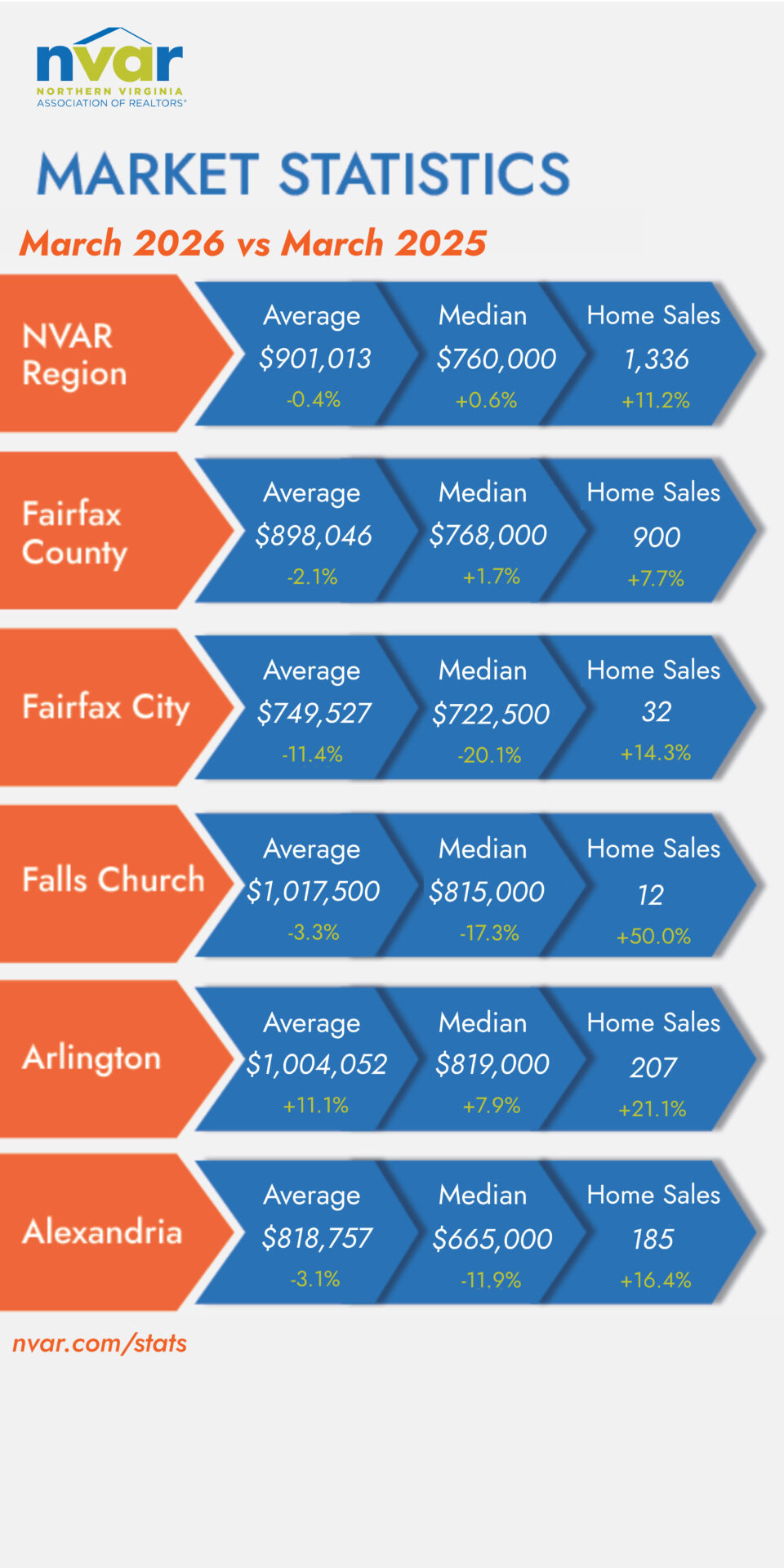

In March 2026, the Northern Virginia market remained active but supply-constrained. According to NVAR’s March 2026 market statistics, the region had 1,336 closings, a median sold price of $760,000, 25 average days on market, 1,938 active listings, and just 1.39 months of supply. That matters if you are trying to sell and buy at the same time, because limited inventory can make finding your replacement home harder.

For Fairfax specifically, NVAR’s jurisdiction-level March 2026 data showed notable differences between the county and the city. Fairfax County posted an average sold price of $898,046, a median sold price of $768,000, and 900 home sales. Fairfax City posted an average sold price of $749,527, a median sold price of $722,500, and 32 home sales, which means city numbers can swing more from month to month because the sample size is much smaller.

Why timing matters more for move-up buyers

A move-up sale is not just about selling high and buying bigger. It is also about managing the transition between two homes, two timelines, and sometimes two sets of financial obligations. In Fairfax, where inventory has remained relatively tight, timing mistakes can get expensive quickly.

That is especially true when mortgage rates are still elevated compared with the ultra-low-rate years many owners remember. Freddie Mac’s PMMS reported a 30-year fixed rate of 6.30 percent on April 16, 2026, and NVAR expects rates to hover around 6 percent through much of 2026. If you are buying a more expensive home, even a short overlap in payments can have a meaningful impact on your monthly budget.

Fairfax owners often have strong equity positions, which helps. Fairfax County budget materials show the average home sales price rose from $790,367 in 2023 to $858,057 in 2024, and that values have increased 105.7 percent from the 2009 bottom. The same county materials also show active residential listings averaged 17 days on market in 2024, which helps explain why many sellers can build equity but still struggle to secure the next home quickly in a competitive environment. You can review that trend in the Fairfax County budget overview and housing data.

Start with your budget, not home tours

Before you tour homes seriously, get clear on what you can comfortably afford. The CFPB recommends starting with lender math so your budget reflects not just the next mortgage payment, but also taxes, insurance, closing costs, moving costs, repairs, and improvements. Their homebuying guidance is especially useful if you are trying to understand the full cost of a move.

If you are counting on equity from your current home, you also need to estimate your likely net proceeds. That means looking at your current mortgage payoff, expected closing costs, and any prep work you plan to do before listing. Your move-up budget becomes much more reliable when it is built on realistic numbers instead of a rough guess.

Preapproval is a helpful next step, but it is not a final loan offer. The CFPB notes in its preapproval overview that preapproval letters commonly expire in 30 to 60 days, and lenders review income, assets, debts, and credit as part of the process. That timing matters if you begin shopping too early and then have to refresh paperwork later.

Selling first is often the safer path

For many Fairfax homeowners, selling first is the more conservative and less stressful option. You know exactly how much your home sells for, you know your likely net proceeds, and you can shop for the next home with a firmer budget. In a market with tight supply and mortgage rates around 6 percent, that clarity can make a big difference.

Selling first can also reduce the chance that you will carry two housing payments at once. If your goal is to move up without stretching your finances, this approach often gives you more control. It aligns with the CFPB’s guidance that people who want to move commonly try to sell before buying another home.

The downside is obvious. You may need a short-term gap plan if your next home is not available right away. That could mean coordinating close dates carefully or preparing for temporary housing while you continue your search.

Buying first can work, but only with reserves

Buying first is possible, but it usually works best when you have strong cash reserves and a very clear financing strategy. You need to be comfortable with the possibility of carrying two mortgage payments for a period of time. You also need room in your budget for two tax bills, two insurance obligations, and overlapping closing costs.

In Fairfax, that overlap can feel especially heavy because inventory remains limited. With around one to one-and-a-half months of supply rather than a more balanced four to six months, buyers may need time to find the right next property. That can leave you owning your current home longer than expected.

If you are considering using equity before selling, the CFPB explains that a home equity loan or HELOC may provide access to funds, but both are secured by your home. A HELOC usually has a variable rate, and missed payments can put your home at risk. That is why this strategy only makes sense if you are fully comfortable with the added obligation.

A middle path can reduce stress

Some move-up homeowners do best with a tightly managed timeline rather than a hard sell-first or buy-first strategy. In practice, that means preparing your current home for market, talking with your lender early, and narrowing your search before you commit to exact dates. The goal is to build flexibility into the process while keeping momentum on both sides.

This matters because financing windows are not open forever. The CFPB notes that once you receive Loan Estimates, you should move quickly, because a lender may close the file as incomplete if you do not express intent to proceed within 10 business days. The CFPB also advises borrowers to make sure a rate lock lasts long enough to reach closing, which is another reason timing deserves close attention.

In other words, the smoothest move-up plans usually begin well before the sign goes in the yard. When your financing, listing prep, and search strategy are lined up together, you are much less likely to feel rushed later.

Don’t overlook Fairfax tax timing

Local tax dates can affect your carrying costs, especially if you end up owning two homes for a short period. In Fairfax County, the current listed 2026 base real estate tax rate is $1.1225 per $100 of assessed value, and real estate taxes are due July 28 and December 5. You can verify the latest details on the Fairfax County real estate tax rates page.

The City of Fairfax is different. Its base rate is $1.055 per $100, and real estate taxes are due June 21 and December 5. On a $750,000 assessed value, that works out to about $8,419 annually in base county tax versus about $7,913 annually in base city tax before any district add-ons or credits.

Those numbers may not decide your move on their own, but they matter when you are planning for overlap. If your sale and purchase happen near a local tax due date, your cash needs may be higher than expected.

A practical Fairfax move-up checklist

If you want to simplify the process, focus on these steps first:

- Confirm whether your home is in Fairfax County or the City of Fairfax.

- Estimate your likely net proceeds after mortgage payoff and closing costs.

- Get updated preapproval and check how long it remains valid.

- Ask your lender what payment level still feels comfortable if there is temporary overlap.

- Build a buffer for taxes, insurance, moving costs, repairs, and closing costs.

- Decide early whether you can tolerate a gap between homes.

- Prepare your current home for market before you need to move fast.

A strong plan does not remove every moving part, but it does make the process far more manageable. That is where thoughtful pricing, polished presentation, and a coordinated buy-sell strategy can help you protect both your time and your equity.

If you are planning a move-up sale and purchase in Fairfax, working with a local advisor who can help you sequence the timing, presentation, and negotiation can make the transition feel much more manageable. When you are ready for a tailored strategy, connect with Vie Nguyen to schedule your concierge consultation.

FAQs

How should Fairfax homeowners decide whether to sell first or buy first?

- Selling first is usually the lower-risk option because you know your sale proceeds before buying, while buying first may work if you have strong reserves and can comfortably handle overlap.

What mortgage timing issues matter for a move-up purchase in Fairfax?

- Preapproval letters often expire in 30 to 60 days, Loan Estimates require timely action, and you should make sure any rate lock lasts long enough to reach closing.

What is the difference between Fairfax County and City of Fairfax taxes?

- They are separate jurisdictions with different base tax rates and payment due dates, so you should confirm where your property is located before planning your carrying costs.

How tight is the Fairfax-area housing market for move-up buyers?

- March 2026 NVAR data showed low regional inventory at 1.39 months of supply, which means buyers may face limited options even if their current home sells quickly.

Can Fairfax homeowners use a HELOC or home equity loan before selling?

- Possibly, but both are secured by your home, and a HELOC usually has a variable rate, so this option works best only if you are comfortable carrying that added risk and payment.

{kind=link}